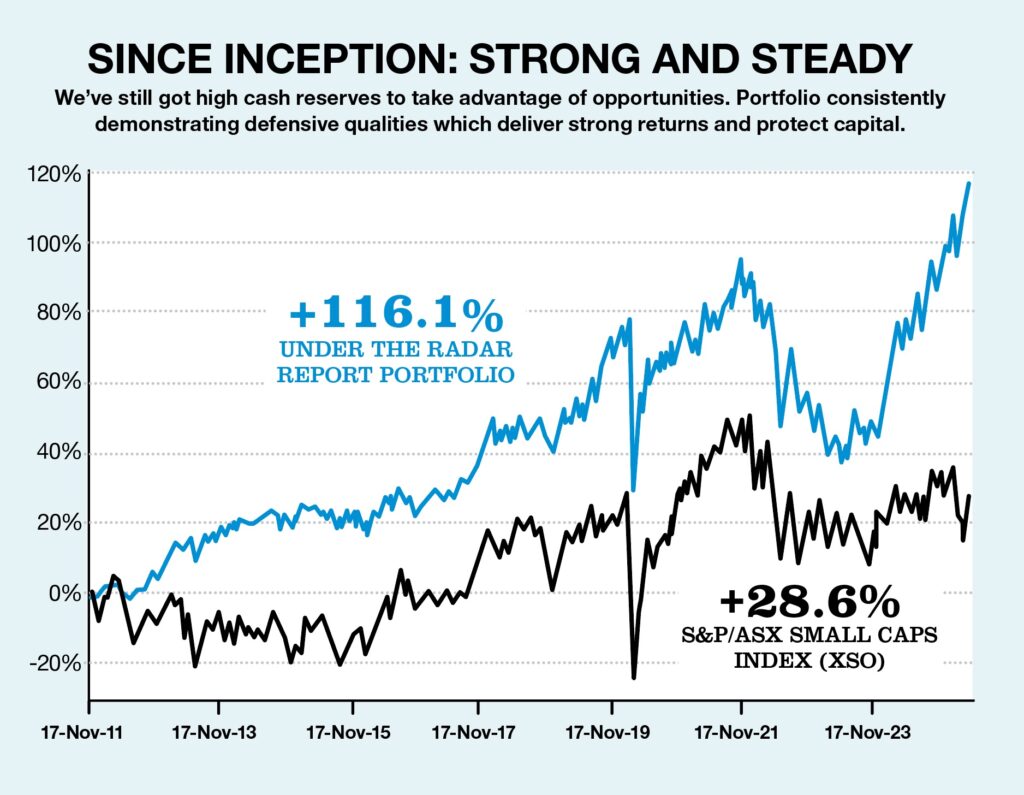

A defensive Small Cap Portfolio managed for Members

Under the Radar’s portfolio has maintained a very defensive stance over the last decade or more. Members may have done a lot better by holding onto some of their big winners, 10 baggers or more. Since this portfolio is managed in public, we avoid oversized positions, demonstrating instead the diversification benefits of a balanced portfolio of quality small cap stocks from Under the Radar Report. This approach also allows us to continually introduce newer holdings, ensuring our performance is not simply based on some lucky calls way back in the past.

No single stock is more than 10% of the portfolio

The portfolio’s strong performance has been led by its largest holdings. These are Austal (ASB), Evolution Mining (EVN), Superloop (SLC) and the GOLD ETF, all of which are triples or close to it. Two have benefited from the current precious metals boom, but while the market as a whole has recovered, gold has not turned down again. This reflects the heightened level of uncertainty, and possibly a recognition that gold’s intrinsic value might be reconsidered. Since we have already taken profits lower down from all these stocks, the big positions could be even larger, but we sleep easily knowing that no single position accounts for more than 10% of the total.

Watch out for end of year selling

When you get significant gains from one stock in your own portfolio, tax considerations will often be top of mind. And in that context, after such a volatile year, we expect some interesting prices towards the Australian financial year end as investors manage their capital gains tax exposure. That could present new opportunities to patient investors, and we intend to be in that mix in June.

Living with losing stocks

It is often harder to think or talk or make decisions about losing positions, whether to cut losses and take the tax deduction against other profits, or hold on for a potential recovery. Professionals think that a 60% hit rate of winning stocks is good. That means that 40% of your selections will go wrong even when you are doing well. The sooner you embrace the possibility of losses, the less they will bother you.

ARN Media (A1N) has disappointed. Our thesis of investing in a market-leading radio network at a reasonable price was badly affected by management’s decision to make an unsuccessful bid for industry rival Southern Cross Media (SXL). Then came weakness in discretionary consumer spending on which advertising depends. While we still think the fundamentals are good, we are not alone in looking for an uptick to exit the stock. Some positive industry noises about advertising revenue may help get a better exit price.

Gale Pacific (GAP) issued an earnings downgrade on Monday, has disappointed repeatedly and has been a value trap. Key US retailer customers have reduced restocking orders due to uncertainty over consumer spending. US tariffs on China hit the bull’s-eye of the company’s manufacturing exposure there, and America’s FY24 sales were almost half the group total. Management is looking to diversify its manufacturing away from China, but that will take time. Inventories increased by 14% over the same period last year at the December half year, which may protect against the immediate impact of tariffs, but prices will have to increase dramatically. At a valuation of less than 20% of sales and 34 cents net assets, to be closely scrutinised at the June year-end, GAP is still too cheap to sell.

Medical Developments (MVP), the latest quarterly cash flow reports have been received more positively, and the stock may ultimately realise some of its promise. Sentiment has turned, but after a long 90 %+ decline, it will take time for the market to regain confidence, though the portfolio’s investment is down a lower 40% due to dollar cost averaging.