Oil and Gas Analysis: 7 November 2025

Download our special report below.

Oil and Gas Analysis 7 November 2025

There is quality at the big end of the sector and we are making money from Woodside Energy (WDS). But not even the biggest lowest cost producers in oil and gas can keep growing in value when oil and gas prices under so much pressure.

Oil Analysis

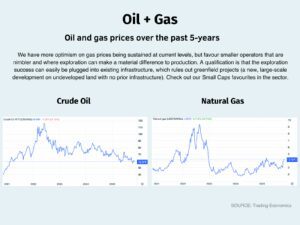

Oil prices have been under pressure all year as weak demand growth has been outpaced by increasing production, causing a consistent surplus and swelling inventories. This has been more than enough to dampen the impact of bullish factors such as the Ukraine-Russian conflict, which has been going for almost four years now, and new sanctions leaving crude prices lower than they have been most of the year.

A cooling global economy and structural trends like improving vehicle efficiency and increasing electric vehicle sales are creating headwinds for fuel consumption. In contrast, total oil output climbed up 5.6 million b/d (12.7%) to 44 mb/d a year ago. This was driven by both OPEC+ and non-OPEC production increases.

This is building inventories and it’s clear that something has to give. Oil demand is inelastic by nature, so rebalancing will have to come from the supply side. That probably means that prices will remain lower for longer to elicit a response from high-cost producers.

Gas Analysis

Gas markets are also characterised by ample supply and moderating prices. One key development is the sustained shift of European purchases from Russian pipeline gas to LNG. However, this pivot to LNG is essentially complete and the continent is entering winter with comfortable inventories.

The increased European demand, steady imports for Japan and South Korea, and opportune buying in South and Southeast Asia have resulted in robust LNG trade flows. The US is now firmly the world’s top LNG exporter and is continuing to increase capacity.

Spot gas prices are far below the peaks of 2022, but they are above longer-term averages and a material supply disruption can impact spot prices. And as the temperature drops in the northern hemisphere, a very cold winter could see big consumers (EU, US and China) looking for additional supply.

Gas is becoming more globalised through LNG but ironically, domestic supply in gas production areas is left deficient. There are big opportunities to generate returns from small cap domestic suppliers. See our small caps publication for details of stocks that have existing infrastructure and are benefiting from rising localised gas prices.

Oil and Gas Stock Updates: 7 November 2025

Please click through to the stock updates for Woodside Energy below.