Download our special report below.

Copper Analysis 9 January 2026

COPPER ANALYSIS: CASH FLOW RAMPING UP FOR MAJOR PRODUCERS

Copper Investment Summary

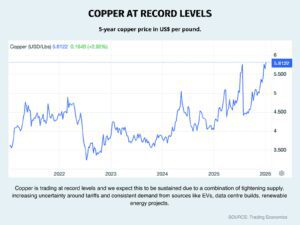

Copper prices have set historic highs for the second time in six months, replicating the price spike in June, July 2025.

The main factor is tightening physical supply, but this is exacerbated by the threat of US tariffs.

One result is for buoyant operating cash flows for copper producers; another is that they are positioning to increase supply in the future. This includes Blue Chip favourites: Rio Tinto (RIO), BHP Group (BHP), and South32 (S32).

Supportive Fundamentals

Fundamentals have been supportive with supply disruptions across major mines in Latin America and Indonesia, while demand consistently climbed, even amid higher prices.

Supply disruptions include a catastrophic mudflow at the Grasberg mine in Indonesia, a tunnel collapse at the El Teniente mine in Chile and the Kakula mine in the Democratic Republic of Congo (one of the newest and largest copper mines) was hit by seismic events and flooding.

The broader narrative of growing copper demand from the global energy transition and associated infrastructure build-out remains, creating a tight market balance. This includes grid buildouts, EVs, renewable power project, and data-centre builds.

Traders are also building positions before the US Secretary of Commerce updates the President on the domestic copper market before June. This is after the on again/off-again 50% tariff on imported copper products from last July have left a legacy of uncertainty.

One result has been higher-than-normal inventories still held in the US; another is lumpy trading. Trade data shows that US copper imports last December jumped to the highest level since July 2025.

The big miners are positioned to benefit.

Corporate activity indicates that major diversified miners see future value in copper.

Copper is now rivalling iron ore as BHP’s most important business and copper assets would have been a key driver of BHP’s unsuccessful pursuit of Anglo American. While Rio Tinto and Glencore have outlined ambitions to double future copper production.