Richard is an experienced equities analyst, stockbroker, and financial editor, having worked for over 30 years in finance.

ASX Lithium Stocks: Riding the Rally, Is It Time to Take Profits?

Riding a wave means knowing when to get on and when to get off. That discipline is exactly what’s guiding our approach to ASX lithium stocks right now.

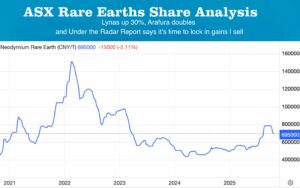

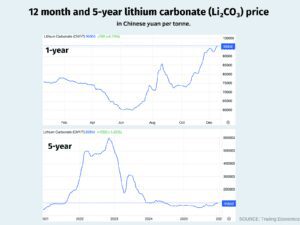

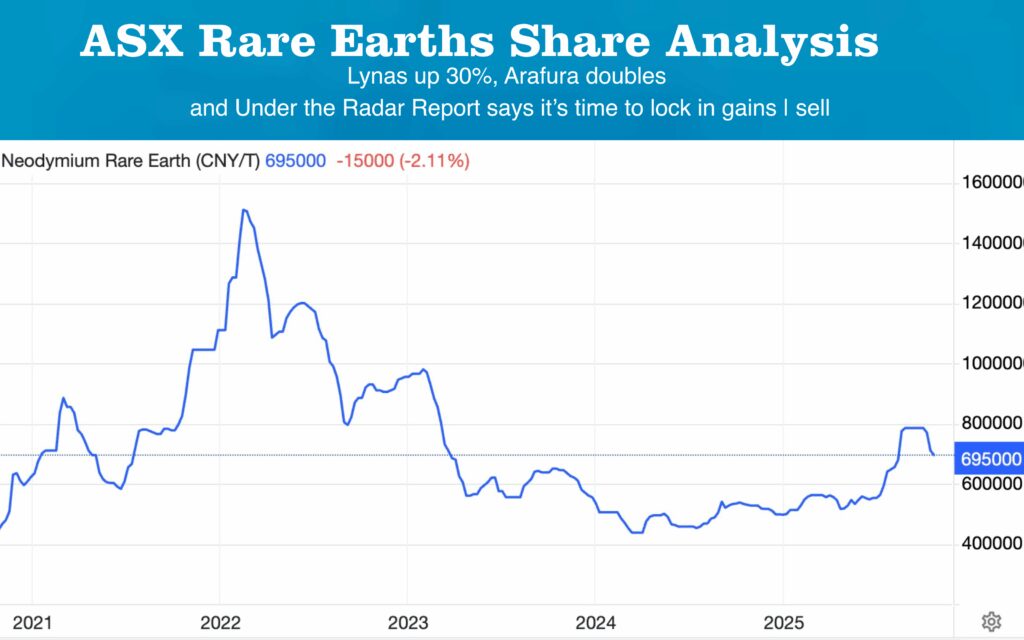

Lithium prices have rebounded sharply over the past year, and the chart below shows just how powerful the move has been particularly when viewed against the longer-term five-year trend. But as the lithium carbonate price charts also make clear, this remains a boom-bust commodity, and equity markets often move faster than the underlying fundamentals.

Readers! Our full stock calls on PLS Group (PLS) and Liontown Resources (LTR) appear below.

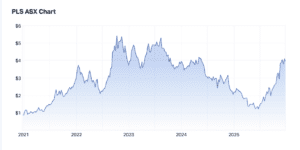

That’s what we’re seeing today. Since Issue 670 in late September, when we downgraded PLS Group (ASX: PLS) to Hold, the stock has surged another 70%, extending a 300% rally in just six months. The move has been driven by a rebound in lithium prices and a rapid shift in sentiment around supply and demand.

We didn’t take profits in the last lithium bull run when PLS climbed as high as $5. But with the share price now back above $4, and lithium equities running well ahead of the commodity itself, the risk-reward equation has changed.

This analysis is not about calling the end of lithium. Lithium prices remain well below their 2021–22 peaks. Instead, it’s about recognising when share prices have moved faster than fundamentals and when disciplined investors should consider stepping aside.

We are not in the business of chasing headlines or jumping on bandwagons.

We are in the business of capitalising on momentum and protecting capital when the balance shifts.

That is how long-term outperformance is built. Subscribe now for full access to our Best Stocks to Buy Now.

Pilbara Minerals (ASX: PLS): Take Profits

Current Price: $3.99

Market Cap: $12.7bn

Net Cash: $292.3m

52-week High: $4.34

52-week Low: $1.07

Risk Rating: 4/5

PLS continues to execute operationally. Lithium recoveries improved to 78.2%, up from 71.6% in the prior quarter, lifting spodumene concentrate production.

Growth projects such as P2000 should continue to increase volumes, while margins are expected to improve through downstream exposure, including the POSCO Pilbara Lithium Solution Co. Ltd (P-PLS) lithium hydroxide facility in South Korea.

Radar Rating:

A sustainable growth profile supported by a world-class deposit. Very high risk, but a large, pure-play, low-cost producer.

Portfolio Risk Rating:

GROWTH. A boom-bust commodity hitting 18-month highs, with the share price now running ahead of the underlying lithium price on the assumption that the improved outlook is sustained.

Our View:

This is an opportunity to take profits.

Liontown Resources (ASX: LTR): Hold, Not Buy

Current Price: $1.44

Market Cap: $4.4bn

Net Debt: $273.7m

52-week High: $1.61

52-week Low: $0.42

Risk Rating: 5/5

Liontown has decisively challenged our previously negative view, rising another 47% since our last update in late September. While we still cannot justify buying a loss-making company with ongoing capital outflows, we are upgrading to a Hold on the improving lithium outlook.

Higher prices should reduce cash burn, but execution remains critical. Liontown must demonstrate:

-

Improved processing efficiencies from underground ore

-

Lower unit operating costs

-

A clear path toward sustainable free cash flow

Radar Rating:

The next quarter is crucial. Underground ore feed must translate into higher recoveries and materially lower costs.

Portfolio Risk Rating:

High risk. Elevated debt and negative free cash flow as the project ramps up. The lithium price rally offers an opportunity to stabilise the balance sheet — but execution risk remains high.

UTRR Lithium Calls

- PLS: TAKE PROFITS

- LTR: Hold

- Risk Profile: High (boom-bust commodity)

Investment Summary

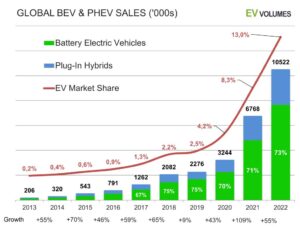

The recent rally in lithium prices has materially improved the outlook for the sector, driven by stronger EV sales, increased support for charging infrastructure in China, and the emergence of energy storage systems as a second pillar of demand.

This improvement in sentiment has delivered a sharp re-rating in ASX lithium stocks. However, equity prices — particularly for PLS Group (ASX: PLS) and Liontown Resources (ASX: LTR) — have moved well ahead of the underlying lithium price, shifting the risk-reward balance.

Lithium remains a boom-bust commodity. While higher prices reduce downside risk and improve project economics, they also incentivise a supply response from Australian hard-rock producers, South American brine operations, and suspended Chinese production, which is likely to cap sustained upside.

Against this backdrop:

-

We are taking profits on PLS following a 300% rally in six months.

-

We have upgraded LTR to Hold, reflecting improving fundamentals but ongoing balance sheet and execution risk.

-

Investors seeking lower-risk exposure may prefer diversified miners such as Rio Tinto (ASX: RIO).

The rally has created opportunity — but at this stage of the cycle, discipline is more important than excitement.

Lithium Stocks Surge: What’s Driving the Rally?

Lithium demand has received a significant shot in the arm, with prices rising more than 30% over the past couple of months.

Initially, the rally was sparked by Chinese supply disruptions, but it has since been reinforced by a meaningful improvement in demand expectations. China has announced plans to double EV charging capacity to 180 gigawatts by 2027, alongside increased support for Energy Storage Systems (ESS) installations.

Add to this:

-

Strong global EV sales

-

Higher lithium refining activity in the final quarter

-

A shift in sentiment from oversupply to potential deficits next year

This change in outlook has more than offset the restarting of CATL’s Jianxiawo (Yichun) lithium mine, which had previously weighed on sentiment.

CATL is not just the world’s largest battery producer — it is arguably the most strategically important company in the global EV ecosystem. When policy and supply signals shift in China, the lithium market pays attention.

Lithium Supply Is Coming. Why Caution Is Still Required.

Despite the recent rally, we do not expect lithium prices to return to the extreme peaks of 2021 and 2022, when a booming EV market was desperate for supply.The reason is simple: the supply response will be significant.

-

Marginal Australian hard-rock producers are capable of restarting operations

-

South American brine producers that mothballed projects can return with sustained higher prices

-

Suspended Chinese production is forecast to come back online

China’s Ministry of Natural Resources has now issued documentation confirming that CATL’s Jianxiawo mine meets regulatory requirements — a major step toward the mining licence being reissued and a return to normal operations. This mine alone accounts for around 6% of global lithium production.

In short, while demand has improved meaningfully, supply will respond — and that response is likely to cap the upside.

EVs and Energy Storage: The Two Pillars of Lithium Demand

More than 70% of lithium demand is driven by EV sales, which are on track to rise 20% to around 20 million units in 2025.

China continues to lead the charge:

-

EV sales up 33% in the first ten months of the year

-

October marked the first time EVs exceeded combustion vehicles, reaching 51.6% market share

The real surprise, however, has been Energy Storage Systems (ESS).

Historically, ESS accounted for around 10% of lithium demand, but it is now emerging as a fast-growing second pillar. Chinese government support has accelerated this trend, although future growth will depend on balancing subsidies with consumer sensitivity to higher prices.

Margins for ESS producers have already come under pressure due to rising lithium carbonate and copper prices over the past 4–5 months, a reminder that even strong demand stories are not immune to cost inflation.

Lithium Shares vs the Commodity: A Disconnect Emerging

Equity prices have run far harder than the underlying lithium price, particularly for our preferred exposures PLS Group (PLS) and Liontown Resources (LTR).

This is a classic feature of commodity cycles:

-

Improving fundamentals spark a rally

-

Equity prices extrapolate perfection

-

Risk rises as expectations outrun reality

That doesn’t mean these companies lack quality, it means discipline matters.

A Lower-Risk Way to Play Lithium

For investors seeking lithium exposure with less volatility, Rio Tinto (ASX: RIO) may offer a more conservative alternative.

Following the Arcadium Lithium acquisition, lithium now represents roughly 3% of RIO’s net asset value, with plans to expand production threefold over the coming years. While not a pure-play, the balance sheet strength and diversification provide an entry point into the theme.

Momentum Is Powerful. Discipline Is Profitable

Momentum creates opportunity but discipline locks in returns.

Yes, ETFs have their place. But individual investors still retain a critical edge: patience combined with selective exposure to small caps, where operating leverage can drive outsized returns.

As the year comes to a close, all of us at Under the Radar Report wish you a very Merry Christmas and a Happy New Year. We’ll be back in 2026 better than ever and kicking things off with a major new Dividend Portfolio.

Stay patient. Stay disciplined. And know when to get off the wave.

Join for full access to our research and get investing today!

Related Articles

Independent ASX Insights

Looking for the next big stock?

Small Companies.

Big Growth Potential.

{kind=link}