Richard is an experienced equities analyst, stockbroker, and financial editor, having worked for over 30 years in finance.

6 ASX Small Cap Turnaround Stocks Ready to Take Off

By Richard Hemming, Under the Radar Report

With guest: Luke Winchester, Merewether Capital

When markets get choppy and investors flee to the safety of blue chips, the biggest opportunities often emerge in the shadows—ASX small cap turnaround stocks that have survived the hard yards and are now poised for a rebound. In this special “three plus three” session, Under the Radar Report’s Richard Hemming and Luke Winchester from Merewether Capital break down six small caps showing renewed momentum, improving financials and the potential to take off .

This is where business models are still being tested, balance sheets really matter, and management teams either step up or disappear. It’s also where you can still find those rare stocks that go from microcap obscurity to genuine wealth-builders.

Along the way, we kept coming back to the same themes: balance sheet strength, capital-light growth and operating leverage.

Here are the six small caps we discussed – and what we’re watching in each. $AHC, $APX, $RTH, $ATG, $CCA, $NCK

1. Austco ASX: $AHC

Nurse Call Systems With Real Operating Leverage

Austco is a nurse call and healthcare technology company that’s been in Luke’s fund since inception.

They sell more than just lights and buzzers in hospital rooms. Austco pairs hardware with software that helps hospitals and aged care providers manage clinical workflow and staff efficiency. That combination – device plus workflow – is where the value lies.

What impressed Luke is how well management navigated a brutal few years:

-

Major customer disruption in hospitals and aged care during COVID.

-

Global chip shortages hitting hardware supply.

-

One of their key ASX peers in the space actually went under.

Austco not only survived, but continued to grow – organically and via acquisition – and has expanded into North America and Asia.

A few things we like:

-

Good management: They made smart acquisitions and have integrated them well.

-

Margins intact: Despite buying lower-margin installation/service businesses, they’ve kept EBITDA margins solid.

-

Contract evolution: Moving from smaller, second-tier hospitals and contracts in the low single-digit millions to larger hospital groups with contracts in the tens of millions.

-

Valuation discipline: Even after a strong share price move, forward earnings multiples still look reasonable if they keep executing.

The order book can be lumpy, depending on when large hospital contracts are signed, so you can’t expect a smooth line up and to the right. But for investors willing to take a 3–5 year view, this is the sort of healthcare tech name that can compound nicely.

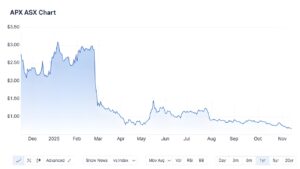

2. Appen ASX $APX

A Fallen Angel With Option Value

Appen is the classic fallen angel. Once a market darling trading around the $40 mark, it now sits at a fraction of that.

So why even bother?

Two reasons:

-

The balance sheet – there’s still meaningful net cash on hand. That buys time.

-

The core problem they solve – providing human-in-the-loop data labelling and oversight for AI models.

At its heart, Appen runs a huge distributed workforce of contractors who annotate and check data for AI systems. When a couple of major US big tech customers pulled spending, the business was smashed. But it has since pivoted towards China, where AI investment and data needs remain intense.

Appen today is:

-

A high risk turnaround, not a defensive compounder.

-

Leveraged to ongoing demand for human oversight in AI – particularly where legal and reputational risk is high.

-

Dependent on management turning aspirational targets (like revenue growth and EBIT margins) into reality, rather than just guidance slides.

For us, the only way to hold a stock like this is to treat it as a small, speculative position:

-

The cash backing provides downside protection to a point.

-

The upside comes if the China segment continues to grow and management delivers anything close to their stated targets.

-

The downside is that growth stalls again and the market loses patience.

It’s not “sleep-at-night” capital, but as an option on a successful turnaround, it’s on the watchlist.

3. RAS Technology Holdings ASX $RTH

Clipping the Ticket on Wagering

RAS Technology sits firmly in Luke’s sweet spot: capital-light, high-margin, B2B software-style economics.

The business has two main segments:

-

Information services

-

Think racing form guides and enhanced data.

-

They take raw racing data, add analytics and context (track, conditions, distances) and sell it to large bookmakers.

-

The goal is simple: help bookmakers drive bettor engagement and turnover.

-

-

Back-end wagering technology

-

They provide the engine that powers the horse racing vertical for online bookmakers.

-

Challenger brands, especially in markets like the UK and Europe, plug into Racing and Sports rather than building in-house capability.

-

The company then clips the ticket on turnover – they don’t take wagering risk, but benefit as customers grow.

-

What we like here:

-

Sticky, B2B customer base – almost every major bookmaker in Australia, plus growing international exposure.

-

Very high gross margins, similar to software.

-

Embedded growth – when a customer like Picklebet starts small and then ramps, Racing and Sports’ revenue grows with them.

-

Operating leverage – revenue growth is now feeding through into EBITDA.

On headline numbers, some investors get nervous because the reported ARR is tied to turnover and isn’t a pure “subscription” number. But if you take the time to follow the revenue line, card-style economics and customer wins, you can see the inflection point.

This is exactly the sort of small cap at the cusp of scale that can re-rate quickly if execution continues.

4. Articore Group ASX $ATG (Redbubble & TeePublic) Can the Turnaround Stick?

Articore is a global online marketplace for print-on-demand merch – t-shirts, mugs, posters and more – connecting independent artists with fans.

It’s also another turnaround story.

The core issues:

-

During COVID, online sales exploded. Management read it as a structural shift and ploughed money into brand and marketing.

-

Google made it harder and more expensive to rely on organic search. Paid performance marketing took over.

-

Costs ballooned, revenue normalised as the world reopened, and suddenly the cost base was too big.

Today the group consists primarily of Redbubble and TeePublic:

-

Redbubble: older brand, more impacted by the shift away from free search traffic.

-

TeePublic: grew up in the era of paid marketing and has held up better.

A new CEO from TeePublic has taken the reins, with a sharp focus on:

-

Gross profit after marketing (not just top-line sales).

-

Tightening up spend.

-

Positioning the business to actually convert revenue into sustainable profit.

The balance sheet isn’t as clean as a simple “net cash” story because of negative working capital. A lot of what looks like cash ultimately belongs to suppliers. Seasonality also matters: the Christmas quarter is critical.

Why it’s interesting:

-

Survival risk has eased – the market no longer prices it as a likely zero.

-

If sales stabilise and grow even modestly, the improved margins could deliver big percentage swings in profit.

-

It’s still a high-uncertainty stock. You’re relying on management to get both marketing efficiency and demand right.

As with Appen, this lives in the speculative bucket, but a well-timed inflection could be powerful.

5. Change Financial ASX $CCA

B2B Payments Riding the Fintech Wave

Change Financial is a B2B payments and card-issuing platform that grew out of a messy corporate history, including assets acquired from the Wirecard collapse.

Strip away the noise and what you have now is:

-

A platform that powers debit and prepaid card programs for:

-

Credit unions and building societies.

-

Fintechs running corporate card or expense card programs.

-

-

A partnership with Mastercard to handle the network side.

-

A model where clients do the hard work of acquiring customers, and Change earns a fee as cards are used.

In other words: win a customer once, then ride their growth.

Key positives:

-

Pure B2B – they don’t take credit risk.

-

Recurring, transaction-linked revenue, with a high proportion of predictable income.

-

Strong growth in active cards on the platform, especially from fast-growing fintech clients.

-

Management has already provided guidance pointing to a move from small EBITDA losses to meaningful EBITDA in FY26.

Like Racing and Sports, this is a capital-light platform where sunk development costs are behind them. As more cards are issued and used, operating leverage kicks in.

Seasonality matters here too – Christmas and peak spending periods are big – but the broader story is one of a small payments platform approaching scale.

6. Nick Scali ASX $NCK

The Small Cap Benchmark for Capital-Light Growth

We finished with a very different kind of small cap: furniture retailer Nick Scali.

On the surface, it looks like yet another retailer at the homemaker centre. Under the surface, it’s a case study in business model design and capital efficiency.

What makes Nick Scali stand out:

-

Showroom model, not traditional inventory-heavy retail. Stores showcase product; not everything is sitting in a warehouse waiting to be sold.

-

Customers pay a large deposit up front (historically around 50%), then the furniture is made and delivered.

-

That means minimal working capital drag – they’re not endlessly funding inventory and waiting months to get paid.

-

It has been founder-led, with a strong focus on balance sheet strength and disciplined expansion.

-

Now rolling out international growth, particularly in the UK, where the market is far bigger than Australia and New Zealand.

Nick Scali is no longer misunderstood – the market now recognises its quality – but it’s still a useful benchmark for what a successful small cap can become.

The dream, of course, is that some of the names we’ve discussed earlier can grow into even a fraction of what Nick Scali has achieved.

Bonus Stock! Hazer ASX $HZR

The Common Threads: What We Look For in Small Caps

Across all these names – from Osco to Change Financial – a few common themes keep coming up:

-

Balance sheet first

Turnarounds like Appen and Redbubble only make sense if they can survive. Net cash, manageable liabilities and honest disclosure matter. -

Capital-light growth

Platforms like Racing and Sports and Change Financial don’t need to build factories or carry huge inventories. Their customers’ growth does the heavy lifting. -

Operating leverage

When revenue grows faster than fixed costs, profits can move very quickly. That’s true for racing data, payments, nurse call systems and online marketplaces. -

Management that learns & adapts

Whether it’s a humble nurse call provider rationalising 800 products down to a few hundred, or a marketplace CEO refocusing on profitable growth, management behaviour is a major signal. -

Embracing some uncertainty

The market pays huge premiums for certainty. If everyone can see exactly what the next three years look like, most of the upside is often already in the price.

To earn outsized returns in small caps, you have to be willing to operate where there’s some uncertainty – but controlled by balance sheet strength and sensible business models.

Small caps aren’t easy, and not every story has a Hollywood ending. But with the right filters – and a long-term mindset – they’re still where many of the most exciting wealth-creating opportunities on the ASX can be found.

Join Now for instant online access

Related Articles

Independent ASX Insights

Looking for the next big stock?

Small Companies.

Big Growth Potential.

{kind=link}