Richard is an experienced equities analyst, stockbroker, and financial editor, having worked for over 30 years in finance.

6 ASX Small Caps Richard and Luke are watching

Six Stocks: from 10c to 70c the small cap picks Richard Hemming and Luke Winchester are backing

There’s been a lot going on in markets over the past few months arguably too much to keep up with.

So instead of trying to cover everything, we’ve gone back to what matters most: stocks.

In this 3+3, I sat down with Luke Winchester from Merewether Capital to run through six ASX small caps we’re watching right now across water, industrials, medtech, defence tech and energy.

Some we own. Some we’re watching. And some sit right on the edge of being interesting.

As oil prices surge in March 2026, Rich and Luke both have a similar investment style:

- instinctively value-oriented

- suspicious of hype

- focused on businesses with durable cash flows and

- they like management teams with real skin in the game.

Let’s talk stocks!

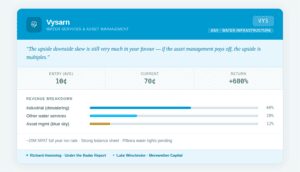

1. Vysarn (ASX: VYS): Water as an Asset

Vysarn is a mining dewatering specialist with blue-sky ambitions to monetise a Pilbara groundwater resource. It is a classic example of how a micro-cap evolves over time.

It started as a relatively simple dewatering business for mining, generating steady cash flow from Tier 1 iron ore customers. That core business still makes up roughly 60% of revenue and earnings.

Entry at 10c and now it is trading at 70c.

But that’s not why the market is interested.

The real story:

- Expansion into broader water services

- And more importantly…

- A move toward water asset management

Think of it like a Pilbara version of the Murray-Darling system where water becomes a monetised asset, not just a service.

“The upside downside skew is still very much in your favour.”

The key tension:

- The core business is low margin

- The blue sky is being priced in

- And monetisation is still years away (FY28–29)

“If the asset management pays off, the upside is multiples, whereas your downside isn’t as much.”

Luke Winchester · Merewether Capital · 3+3 Series

UTRR View:

This is no longer a cheap stock.

But it is one where:

- Downside is supported by a real business

- Upside comes from a potentially transformative asset

👉 Watch closely or build a small position if you want exposure

We have introduced monthly pricing. Same research and advice, without the year long commitment.

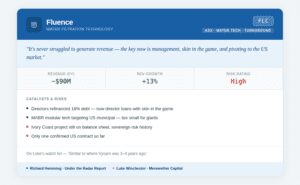

2. Fluence (ASX: FLC): Turnaround in Motion

From distressed debt to director skin-in-the-game. FLC is a US-pivoting water tech company with $80–95M revenue and a cleaner balance sheet. Fluence is almost the mirror image of Vysarn. Where Vysarn has surged, Fluence has spent years disappointing investors.

What’s changed:

- Balance sheet repaired (distressed debt removed)

- Management now has skin in the game

- Strategic pivot to modular water systems (MABR)

The opportunity is clear — particularly in the US municipal market.

But execution remains the key risk.

“The key now is management… skin in the game is huge.”

The reality:

- ~$90M revenue base (solid)

- Historically low margins + poor cash flow

- Still early in turnaround

“The technology suggests something real and they have a modular niche that the giants won’t touch.”

Richard Hemming · Under the Radar Report · 3+3 Series

UTRR View:

This is:

- We are positive on this stock. Get our full research on Fluence (FLC)

- But one to watch closely

👉 If execution improves, this could look like Vysarn three years ago

See 5 of our favourite ASX Small Caps to buy now.

3. Laser Bond (ASX: LBL): Industrial IP Play

Laser Bond is a rare ASX manufacturer with real IP.

They specialise in:

- Extending the life of heavy equipment

- Reducing replacement costs

- Improving ESG outcomes

What stands out:

- 58% gross margins (exceptional for industrials)

- Strong underlying demand

- Capacity — not demand — has been the constraint

What’s changing:

- Labour bottlenecks easing

- Second shifts being rolled out

- Licensing model gaining traction

The swing factor:

- A $2.3M Komatsu licensing deal

- Could materially lift earnings if delivered

“The business is in the best position it’s ever been fundamentally, the capacity is there, the labour pathway is there.”

Luke Winchester · Merewether Capital · 3+3 Series

UTRR View:

- Solid business

- Improving fundamentals

- But don’t overpay

👉 This is a discipline stock — not a momentum trade

4. Nanosonics(ASX: NAN): Quality at a Price

Nanosonics is one of the highest-quality businesses on the ASX.

Why:

- Global franchise

- Recurring revenue model

- Strong margins

- $160M cash

It’s the classic razor-and-blade model:

- Sell the device

- Monetise consumables

The debate:

- It always looks expensive

- But rarely actually is (for its quality)

“You’re never going to get it at a bargain basement price.”

The opportunity:

- Slower rollout of “Chorus” has cooled sentiment

- Multiples have compressed to ~20–25x

“Chorus is effectively free at this valuation.”

Richard Hemming • Under the Radar Report • 3+3 Series

UTRR View:

- A sleep-at-night stock

- If you buy at the right price

👉 This is about quality + patience, not timing perfection

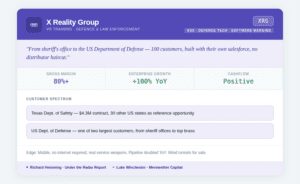

5. X Reality Group (ASX: XRG): VR Training Disruptor

This is one of the more left-field ideas, but potentially one of the most interesting.

Originally indoor skydiving, the business has pivoted into:

Operator XR:

- VR training for police + defence

- Real-world simulations

- Software-driven margins

The numbers:

- 100+ customers

- 80%+ gross margins

-

100% growth

“From a sheriff’s office to the Department of Defence.”

What’s compelling:

- Built by people who understand the end user

- Mobile (no fixed installation required)

- Recurring revenue

“It’s like the next Catapult. Only instead of elite sports teams, it’s police with goggles.”

Richard Hemming • Under the Radar Report • 3+3 Series

UTRR View:

- Early stage

- High growth

- But now cash flow positive

👉 This is a genuine small-cap growth story

6. Amplitude Energy (ASX: AEL): Gas

With energy back in focus, Amplitude stands out. Please see our full update on our member dashboard.

Full update out 26 March 2026

Key points:

- Strong production (Otway Basin)

- ~$200M+ revenue

- Short-term contracts → leverage to spot pricing

The risks:

- Exploration misses (e.g. Eleonora)

- Operational hiccups

- Commodity volatility

UTRR View:

- Higher risk than majors

👉 A position sizing stock, not a core holding. NOTE: There has been a big price move since filming this video. A full member update is available on our dashboard.

Across these six stocks, a few themes stand out:

- Don’t overpay for growth

- Look for real businesses underpinning valuation

- Be patient with long-dated blue sky

- And always manage risk through position sizing

If you’re not already a member, this is exactly the kind of analysis we provide every week:

✔️ Best ASX small caps to buy now

✔️ Full valuation breakdowns

✔️ Risk ratings

✔️ Portfolio strategy

We have introduced monthly pricing for your convenience.

please note: This is general information only and not personal financial advice. Please consider your own circumstances before acting.

Related Articles

{kind=link}