ASX Dividend Stocks Paying 7.5%: ELD & AMC

The recent Federal Budget sent a clear signal to investors: dividends and superannuation are here to stay. With tax benefits intact and the cost minimisation advantages of super untouched, now is the perfect time to revisit why dividend-paying stocks should form the backbone of your portfolio.

Buy Cheap and Be Patient: The Core Philosophy

At Under the Radar, our investing philosophy is straightforward and it’s been proven to work.

The biggest driver of your investment return is the price you pay.

Everything else flows from that. Buy Cheap and Be Patient means waiting for out-of-favour stocks to be mis-priced, then holding long enough for the market to recognise their value.

This isn’t just theory. Three of our recent dividend portfolios, measured to January 2026, have returned an average of 27% versus the ASX All Ordinaries return of just 2%. That’s a 25 percentage point gap. The direct result of disciplined stock picking focused on dividend quality and entry price.

Why Dividends Change Everything

There’s a crucial distinction between investing and speculation, and dividends are the difference. When a stock pays you income, short-term price swings become far less threatening. You don’t need to sell to realise returns, and if the stock is held inside superannuation, you’re sheltered from capital gains tax entirely.

That’s a powerful combination: income, tax protection, and the patience to let compounding do the heavy lifting.

Stock Picks: What We’re Watching Now

CSL Limited: 4%+ Yield

CSL is a name every Australian investor knows, but it’s now entering territory where the yield makes it genuinely interesting at over 4%. For a large-cap quality compounder, that’s a meaningful starting income base.

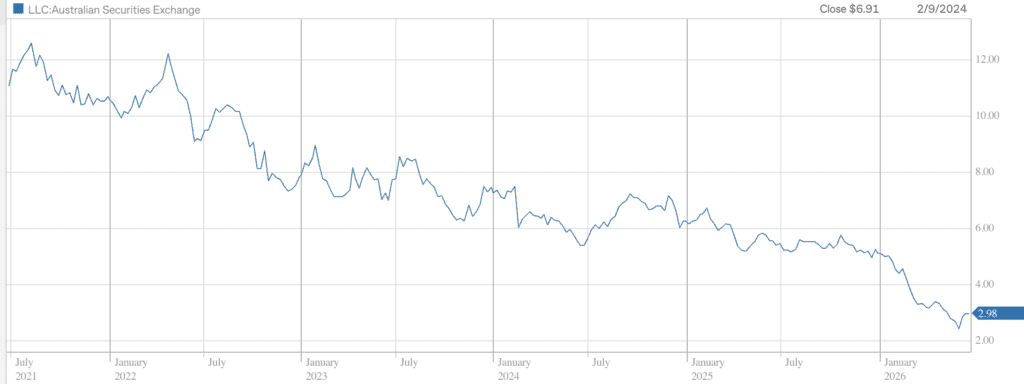

Elders (ASX: ELD): 6.5% Yield ⭐ Standout Pick

Elders is our standout pick right now. At a 6.5% yield, it screens as deeply out of favour yet the underlying business is anything but fragile.

Yes, Elders has cyclical earnings. But it is the dominant domestic player in agricultural services by a considerable margin, which substantially lowers the risk profile. When you’re the clear market leader in a sector with high switching costs and recurring customer relationships, cyclicality is manageable.

On the balance sheet front, the picture is improving rapidly. The $196 million sale of the Killara feedlot is due to complete shortly, which will materially reduce debt. While the Delta acquisition has increased leverage in the near term, Elders generates earnings from a wide diversity of sources — this diversification underpins the sustainability of the dividend.

The compounding case for Elders is compelling. If dividends grow at 10% per year, a reasonable assumption for a dominant franchise, you would double your dividend income in under seven years. Add franking credits on top of that, and the after-tax return becomes even more attractive. In a superannuation environment, you could theoretically hold this stock indefinitely without a CGT event.

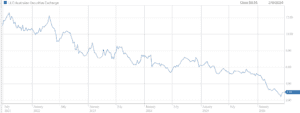

Amcor (ASX: AMC): 7.5% Yield

Amcor is a more complex thesis, but the yield tells you the market has priced in significant risk and we think the risk/reward balance is currently favourable.

At a 7.5% yield, the market is clearly worried, and there’s a legitimate reason: Amcor carries $14.3 billion in net debt. Post the Berry Global acquisition integration, expected EBITDA is $3.7 billion, putting leverage at just under 4x, right at the edge of acceptable corporate leverage ratios.

But here’s what the bears are missing: synergies from the Berry deal are coming in ahead of expectations, and the company continues to generate solid free cash flow. That cash flow is what supports the dividend.

The key risk to monitor is a US consumer slowdown. Amcor’s packaging is deeply tied to consumer packaged goods, and if the US economy slows materially, earnings assumptions would need to be revised. Disruption from broader geopolitical factors is also baked into current estimates.

That’s precisely why you’re being paid 7.5% to own this stock. The yield compensates you for bearing that uncertainty.

The Out-of-Favour Stock Advantage

There’s an added dimension to buying quality stocks when they’re deeply out of favour at the large-cap end: passive fund momentum. When a stock turns and re-enters favour, index and passive funds are forced to buy as its weight increases. That buying pressure accelerates your returns on top of the income you’ve already been collecting.

The pendulum effect is real — and it magnifies gains for patient investors who got in before the crowd.

The Bottom Line

Dividend investing done well is not passive or boring. It requires disciplined analysis of balance sheets, sustainable payout ratios, and critically entry price. But when you get it right, the combination of income, franking credits, superannuation tax benefits, and compounding growth is difficult to beat.

Elders at 6.5% and Amcor at 7.5% are the kinds of yields that, in a world of elevated valuations, genuinely stand out. The swings will come, but if you’re collecting dividends, the swings don’t matter nearly as much.

That’s the real edge of stock picking. Click here to join today.

—

*Richard Hemming is the founder of Under the Radar Report, specialising in small and mid-cap ASX stocks. This article is general information only and does not constitute personal financial advice.*

Related Articles

Start Investing

Flexible access to expert ASX research, without the long-term commitment.

Small Caps Research

Uncover high-growth opportunities

$69.70/mo

Blue Chip Research

Build a strong, reliable core

$22.70/mo

Richard Hemming

Founder, BA (Econ, maths statistics), FSIA

Richard is an experienced equities analyst, stockbroker, and financial editor, having worked for over 30 years in finance.

{kind=link}