Richard is an experienced equities analyst, stockbroker, and financial editor, having worked for over 30 years in finance.

Stocks on Sale for 30 June: 4 Fallen Angels We’re Buying

30 June is upon us and the inevitable selling is materialising. Some investors are locking in losses to offset capital gains. Now is the time to take advantage. We’ve done a number of screens looking for Fallen Angels. We’ve come up with 4 of them to think about this week. Who knows, you might even buy them? We have.

Picking stocks is about reaping bigger rewards for longer. You want that compounding effect. Stocks you pick within 12 months can vary in performance. It is over time where you experience the big growth.

Stocks we picked 12-24 months ago have returned on average 60-70%. It is over time where you experience the big growth.

We will be showcasing them this week in our small caps newsletter.

Quality On Sale

What we’re always trying to do is to increase the quality of our portfolio by buying stocks that we like that are On Sale. This is the perfect time to do it!

The key is not to go too hard. Small bites only if these stocks match your risk profile. Remember, there are a lot of what we call “Stale Bulls” in there, which means investors who’ve bought in at higher prices and are gun shy. Another factor is the dividend.

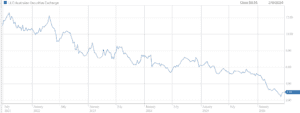

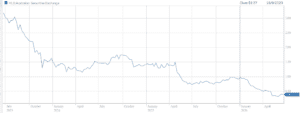

High profile stocks hit the hardest: $CSL, Cochlear $COH, Lendlease $LLC & $ASX. Of these $LLC is our favourite, though all are bouncing off lows.

Buying for the dividend: Lendlease $LLC

- Recent selling due to having fallen out of the S&P/ASX100 Index, i.e. not related to fundamentals;

- 5% fully franked dividend yield;

- Has reaffirmed Core development & construction earnings guidance 30 cents a share – underpinning 19 cent dividend for FY27;

- Selling assets to reduce debt;

- Net debt of $3.2bn – definitely on the high side at 4x;

- Outlook fy27 positive with an $8bn contract backlog.

A Blue Chip that’s turned into a Small Cap: Healius $HLS

We took profits a couple of times much higher at $1.60 a couple of years ago and at about $1 last year, but now, at below 40 cents, the stock is a third of its level at the start of the year.

- A key reason is that $HLS is not getting strong govt tailwinds, with no new funding in the federal budget;

- Recent trading update included 20% downgrade to fy26 earnings;

- But look at the value! Trading at less than a quarter of sales; let’s say about $1.4bn; this stock trades on $300m;

- Demand for pathology is not discretionary;

- The balance sheet a challenge, $40m debt offset by $51m in cash; but net current liabilities of $187m – money is tight;

- Labour costs 50% of revenue but reducing;

- Too big to fail as Australia’s second biggest pathology provider with 25% market share, behind Sonic Healthcare $SHL;

- Paul Anderson is a relatively new CEO – has a good record.

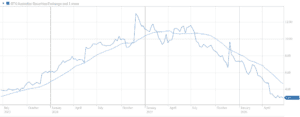

The software apocalypse! Gentrack $GTK or Hansen $HSN?

- both software billing systems for major utilities

- $GTK will be full of stale bulls for while – it does have diversification with the airports business;

- But $HSN has diversification across both energy, water utilities and telecoms;

- $HSN still getting benefit of powercloud acquisition in Germany;

- $HSN contract wins across different sectors in the US;

- $HSN is even more mission critical because has bigger customers;

- Bulk of $HSN technology is on premise, which means contracts are stickier.

{kind=link}